What are closing costs and how much are they? An itemized breakdown of closing costs in MA

The question on closing costs and how much to budget for it is a common one often brought up by my buyers.

Sticking to professional limits, my response would be typically a ballpark estimate, followed by advice that they seek clarity from their lender. This is still the right approach… albeit starting today, I’m ready to give better answers! 👌

And I’m really excited about this post because I’ve prepared well for it. Yes I did! I literally printed 10 American Land Title Association (ALTA) statements by various lenders and closing attorneys and studied the line items in order to put together a coherent post on this topic.

I further had it sent to my trusted Loan Officer, Katherine Castro Eardley, to check if anything was amiss. Katherine - God bless her - made edits and even had them forwarded to her Manager for additional inputs before getting back to me. Disclaimer: this is not a sponsored post; the people I work with simply go above and beyond.

From the best of Joan and Katherine, we hope you find this enlightening!

What are Closing costs?

Ok first, for those unfamiliar with housing transactions, the Closing refers to the final step in the process - literally the last day - where documents are signed, monies exchanged and the transfer of ownership happens.

Beyond the sum of money agreed to for the sale of property, there are other costs involved. These “other costs” are closing costs- a summation of expenses incurred by the Buyer and the Seller throughout the housing transaction and for the necessary completion of it.

Sellers are less concerned about closing costs than Buyers, because theirs are more predictable. More on that later.

Buyers however (referring to the majority who take a loan for their purchase), face a more variable closing cost and yet are often without the full picture until late into the transaction (read: a week before the Closing). Don’t get me wrong, buyers do get a rough idea along the way, courtesy of banking regulations that mandate they be sent the:

Loan Estimate, within 3 business days after applying for the loan;

Closing Disclosure, least 3 business days before the Closing

But do you see the knowledge gap?

The Loan Estimate comes only after loan application… at that point the lender would have pulled a hard credit enquiry. How then can buyers shop with multiple lenders if each application deducts credit?! How many hard enquiries can one with a credit score of 650 afford? Two hard enquiries is one too many.

Actual closing costs are rarely lower than the initial estimates. The Closing Disclosure has the actual figure… but hey, what ya gonna do 3 days before the Closing.

If communications were poor and expectations ill-managed… sticker shock and unhappiness only. 😖

Would reading this post allow you to know exactly what your closing costs will be before applying for a loan? No, because variable costs exists between lenders and attorneys etc.

But this will be be close. No pun intended.

This will provide a heads up of inevitable costs, while knowing what questions to ask and to whom to ask to figure out the variable ones. Figuring out inevitable costs alone would probably give you a grasp of 85% of closing costs.

What better way to start than to begin at the end? 😉

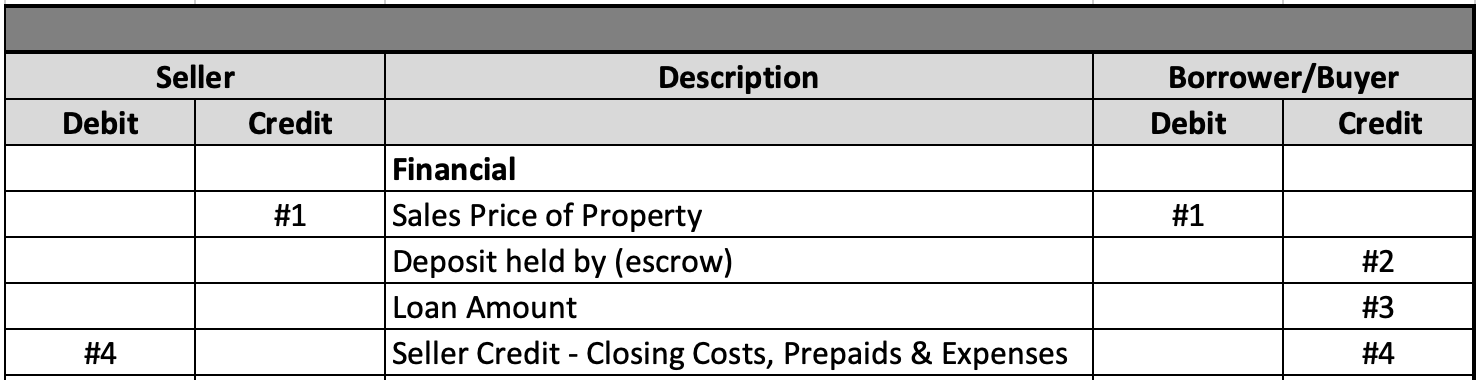

For that, we’ll look at the ALTA Settlement Statement (usually just referred to as “ALTA”). This is a standardized document that is not even shared until the Closing - at which point you’d be seeing it for the first time and signing it.

Behold now, THE RECEIPT!

The sample below is taken from ALTA’s webpage and edited to reflect a typical MA transaction. I’ve numbered the items and placed similar ones in fields where values will be the same.

Part 1

What are closing costs for Buyers?

The closing costs for a Buyer are reflected in the “Debit” column of the ALTA, excluding the Sales Price of Property (#1). So let’s look at #5 onwards.

Prorations/Adjustments

#5 City/Town Taxes

Are assessed by the quarter per the below schedule.

Q1: 1 July 2021 - 30 Sept 2021.

Q2: 1 Oct 2021 - 31 Dec 2021.

Q3: 1 Jan 2022 - 31 Mar 2022.

Q4: 1 Apr 2022 - 30 June 2022.

If the Seller of the property has paid taxes for the quarter of which the Closing occurs, the Buyer would pay a prorated share of that quarter’s taxes. i.e. If Closing is on 8 Jan, you would be responsible for prorated taxes from 8 Jan - 31 March.

#6 HOA/Condo Fee

If applicable. Proration would be from date of Closing to date of which Seller has paid fees. In a condo with regular monthly fees, that would be e.g. 8 Jan - 31 Jan.

Loan Charges to (lender co.) & Other Loan Charges

Only applicable if you’re financing the purchase with a loan. Cash buyers please ignore and skip to #18.

Here’s where you’d want to seek clarity with the Lender when shopping for your mortgage. While the interest rate quoted is often a key factor in picking the Lender, it would be good to have an idea of the expected costs that accompany your loan.

Items #7 - #14 are what I commonly see- and items you can expect on your ALTA. Remember at the end of the day these vary between Lenders. Some of these items are dependent on the size of your loan and downpayment.

#7 Origination Fee

Fee that the Lender charges for making the loan. It would be based on the size of loan.

Ask the Lender for an estimate.

#8 Prepaid Interest from (closing date) to (date)

Applicable if you’re not closing on the last day of the month. You’d pay a prorated share of interest from the date of Closing to the end of the month.

#9 Appraisal Fee

Lender would send an independent 3rd party appraiser to appraise the value of the property.

$425 - $740

#10 Credit Report Fee

$14 - $89

#11 Flood Certification Fee

Lender would have a 3rd party company provide a Flood Certificate that determines whether or not your property is in a flood zone. You could read my posts on “What to do when your property is suddenly in a flood zone” and “How to remove a flood determination”.

$8 - $11

#12 Homeowner's Insurance Premium

Lenders would require a year’s premium to be paid in advance.

Quote varies according to insurance provider.

#13 Points

Also known as Mortgage Points or Discount Points. These are fees that a buyer pays a Lender in exchange for a reduced loan interest rate. 1 point equals 1% of the loan amount. Depending on the Lender, this does not have to be a whole number.

Check if your quoted rate is contingent upon points paid.

#14 Tax Service Fee

Fee that Lender pays a 3rd party to verify that that there are no outstanding tax bills.

$72 - $98

#15 Other Fees

No, the ALTA will not show this as “Other Fees”- that would be too sketchy :)

Here’s where you’d ask the Lender what else should you expect to pay. In the ALTAs that I’ve reviewed, other line items may include Underwriting Fee, Compliance Report, MERS Registration Fee, Verification Fee, Documentation Fee (yes, this is sketchy).

Note if you plan to close on the last month of a fiscal quarter- September, December, March or June. In addition to the prorated property taxes for that quarter itemized in #5, you’d also be required to pay taxes for the next quarter. i.e. If you close on 1 March, you’d see 1 - 31 March proration in #5, followed by 1 April - 30 June in this section.

Impounds

This is an escrow account that is set up by the Lender to pay property-related expenses. A portion of your monthly mortgage payment contributes to this account and is used by the Lender to make necessary payments.

#16 Homeowner's Insurance

Yes, on top of #12 where a year’s premium is collected, these additional months’ payment also go to escrow. If you do not plan for a 20% downpayment, you’d almost certainly be required by the Lender to escrow insurance. The exception: purchasing a Condo. Some Lenders may waive requirement if the Master Insurance is deemed to have sufficient coverage.

Typically 2-3 months’ premium.

#17 Property Taxes

Yes yet another item on property taxes. This is on top of #5 where you pay the prorated share of the tax quarter and if applicable, #15 for next tax quarter.

Typically 2-3 months’ taxes.

Title Charges & Escrow / Settlement Charges

#18 Title - Settlement Agent Fee

In the majority of circumstances, the Buyer’s Attorney would also represent the Lender as the Settlement Agent (also known as the “Closing Attorney”). Buyers would see their attorney’s fees in this line. Of course you may enquire about fees prior to engaging the latter.

$500 and above.

#19 Owner's Title Insurance (Optional)

In MA it’s common for attorneys to own a title insurance agency or be affiliated with one, so this would likely be a quote provided by the Buyer’s Attorney.

Premium is based on purchased value of property.

#20 Title - Lender's Title Insurance

Same as above, except premium is based on loan amount.

#21 Title Search

$200 - $325

#22 Town Municipal Lien Certificate (MLC)

Legal document that lists all taxes, assessments, water and sewer charges owed to the town on a parcel.

$50

#23 Wire Fees

Because Venmo is not accepted. Unfortunately.

$30 - $65

#24 Survey/Plot Plan

$125 - $150

#25 Others

Like #15, here’s where you could ask your attorney if there would be other line items. Some additional ones I’ve seen: Closing Protection Letter (CPL), Homestead Preparation Fees.

Government Recording and Transfer Charges

These are necessary for legal documents to be recorded at the relevant Registry of Deeds.

#28 - #31 Recording Deed, Mortgage, Municipal Lien Certificate, Declaration of Homestead

The MA Registry of Deeds fee schedule applies.

Deed: $155

Mortgage: $205

Municipal Lien Certificate: $80

Declaration of Homestead: $35

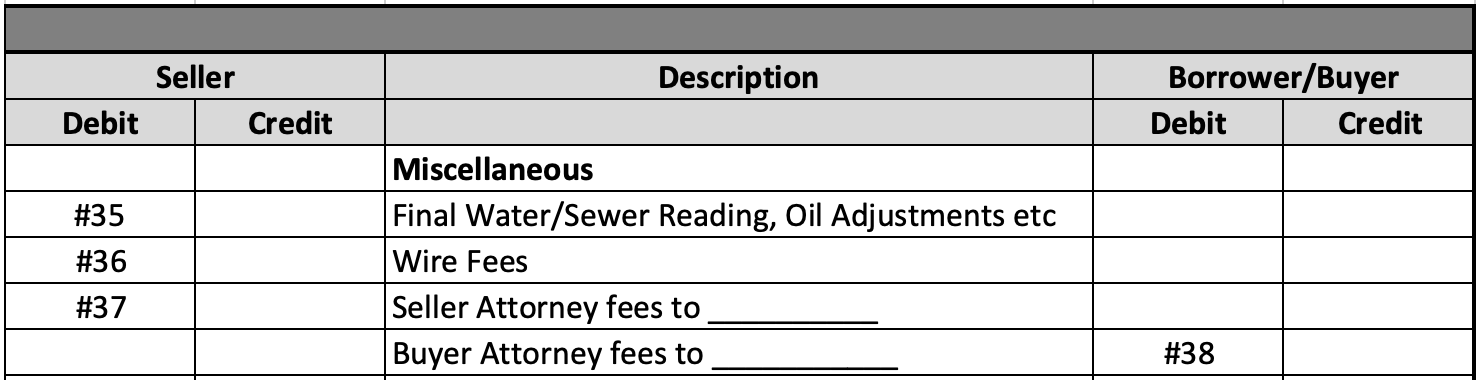

Miscellaneous

Did the Buyer agree to pay for the Smoke/CO inspection? Credit the Seller $X at Closing? This is where other monetary terms of the contact are reflected.

#38 Buyer Attorney Fees

Some law firms charge the Settlement Agent’s fee and a separate Buyer Attorney’s fee. Other times there are Buyers who elect to use different attorneys - one for the Closing and another for Buyer’s representation.

$500 and above

Part 2

What are closing costs for sellers in Massachusetts?

The closing costs for a Seller are reflected in the “Debit” column of the ALTA, with notably fewer items as compared to the Buyer’s list.

Financial

#4 Seller Credit - Closing Costs, Prepaids & Expenses

Any amount of credit to Buyer agreed to during the transaction, e.g. at Buyer’s terms in Offer, repair costs after home inspection.

This amount is impossible to predict unless you’d listed your property for sale with a credit disclosure e.g. replacement costs for new septic.

Commission

#26 - #27 Real Estate Commission to Seller Agent's Brokerage and Buyer Agent’s Brokerage

I’m addressing both items together as they are expenses that should have been discussed prior to the signing of the Exclusive Right to List contract between you and your listing agent. Don’t worry, when you and your Agent discussed the latter’s commission it would have already included the commission to the Buyer’s Agent i.e., you’re not paying your Agent AND separately paying the Buyer’s Agent. You pay one commission, and that commission gets split at the Closing between two Agents.

4 - 6% of sale price

Government Recording and Transfer Charges

#32 Recording 6D, Trustee Cert

If you’re selling a condo, recording the 6D certificate (a document that affirms all condominium fees are paid in full up to the current month) is necessary. If ownership was held in a Trust, a Trustee Cert would be recorded.

The MA Registry of Deeds fee schedule applies.

6D (Under “All other documents”): $105

#33 Tax stamps to Commonwealth of Massachusetts

All MA counties with the exception of Barnstable County: $2.28 per $500 of sale price, rounded up

Barnstable County: $3.24 per $500

e.g. $825,123 sale in Acton (Middlesex County): $825.5 X $4.56 = $3,764.28

Miscellaneous

#35 Final Water/Sewer Reading, Oil Adjustments etc

Utility bills up to the date of occupancy.

#36 Wire Fees

$50

#36 Seller Attorney Fees

Enquire about fees prior to engagement.

$650 and above.

That’s all folks!

Acknowledgements

To Katherine,

For availing yourself on Sunday evenings; for teaching me, watching over my clients… and everything in between.

For the good that you have given, I know you’ll be rewarded in many ways.

Katherine Castro Eardley

Loan Officer, Guaranteed Rate

Email: katherine.castroeardley@rate.com

Mobile: 978-973-7115

Reviews

Calculate Massachusetts Closing Costs

Want an excel to calculate your closing costs? Leave me your name and email and I’ll send one to you!